A standard clause in every venture capital term sheet is about liquidation preferences. This blogpost explains how liquidation preferences work in practice, what forms of liquidation preferences exist, and what’s commonly used in the Dutch venture capital market place.

Guest blog by Sjoerd Mol, attorney-at-law at Benvalor

What are liquidation preferences?

Liquidation preferences give preferred shareholders the right to receive an amount of the proceeds from a sale or liquidation of the company before the common shareholders are entitled to receive anything.

Sometimes entrepreneurs think a liquidation preference only applies in case of a bankruptcy or a wind down of the company, but this is not the case. It is usually tied to events (usually defined as ‘liquidity events’ or ‘liquidation events’) where the shareholders receive proceeds for their equity in a company, including mergers and acquisitions. As a result, the liquidation preference determines allocation of proceeds in both good and bad times.

A liquidation event is usually defined along the lines of the following: a liquidation, legal merger, legal division, sale or redemption of shares or issuance of shares leading to the existing shareholders having less than 51 percent of the controlling rights in the Company, or the sale of all or nearly all of the business operations or assets of the Company.

There are basically two forms of liquidation preferences:

Non-participating liquidation preferences or simple liquidation preferences

These give investors the right to get paid back the amount of their investment in case of a sale or liquidation of the company. After they have received their invested amount, the remainder will be paid to the common shareholders. This form is only used if the preferred shareholders have the right to convert their preferred shares into common shares (which is the standard in the US) or have the right pursuant to their preferred shares to either opt to be paid back their investment or to share in the proceeds as common shareholders (more common in Dutch VC deals, no need to convert, but this is not possible in all jurisdictions). For the latter, please consider the following language:

In the event of a Liquidation, the Exit Proceeds shall be distributed among the Shareholders at the option of the Meeting of Preferred Shareholders by:

- paying the Preferred Shareholders first an amount equal to their Total Investment [plus any accumulated and unpaid dividends] and thereafter any remaining proceeds to the holders of Common Shares in proportion to the nominal value of their Shares; or

- distributing the proceeds among all Shareholders in proportion to the nominal value of the Shares held by each Shareholder.

Participating liquidation preferences

These give investors the right to receive their invested amount in case of a sale or liquidation of the company and, on top of that, share in the remaining proceeds with the common shareholders on a pro rata parte basis. This is also called the double dip, which is obviously more favorable for investors. Such a provision normally looks like this:

In the event of a Liquidation, the holders of Preferred Shares will be entitled to receive in preference to the holders of Common Shares payment of an amount equal to their Total Investment [plus any accumulated and unpaid dividends]. Thereafter, any remaining proceeds will be distributed among all Shareholders in proportion to the nominal value of the Shares held by each Shareholder.

Then there are multiples, dividends and caps. Under a multiple liquidation preference, the investor is paid out a pre-defined multiple of his invested amount before the remaining proceeds are distributed. Multiples may vary from 2 to 4 times the invested amount.

The liquidation preference, whether simple or participating, can be further improved for the investors by increasing the preferred repayment amount with accrued and unpaid dividends. A cap limits the payment to the investor under a participating liquidation preference to a certain amount. Please note the following sample provision, which is usually tied to a conversion right for the investor:

After payment of the liquidation preference to the holders of the preferred shares, the remaining proceeds shall be distributed among all Shareholders in proportion to the nominal value of the Shares held by each Shareholder, provided that the holders of Preferred Shares will stop participating once they have received a total amount per share equal to [X] times the invested amount [plus any accumulated and unpaid dividends]. Thereafter, the remaining proceeds shall be distributed among the holders of the Common Shares.”

Why do investors want liquidation preferences?

Liquidation preferences are primarily meant to provide investors with protection against their downside risk, at the cost of the other shareholders. If the company is not lifting off and after years of struggling is sold at a very low valuation, liquidation preferences give the investors the right to get their money back first.

In those circumstances, there is usually nothing or very little left to share among the common shareholders. Moreover, provided that the investors have a participating liquidation preference, they will, in addition to the aforementioned downside protection, obtain upside potential in the event of a successful sale or merger of the company.

How does this work in practice?

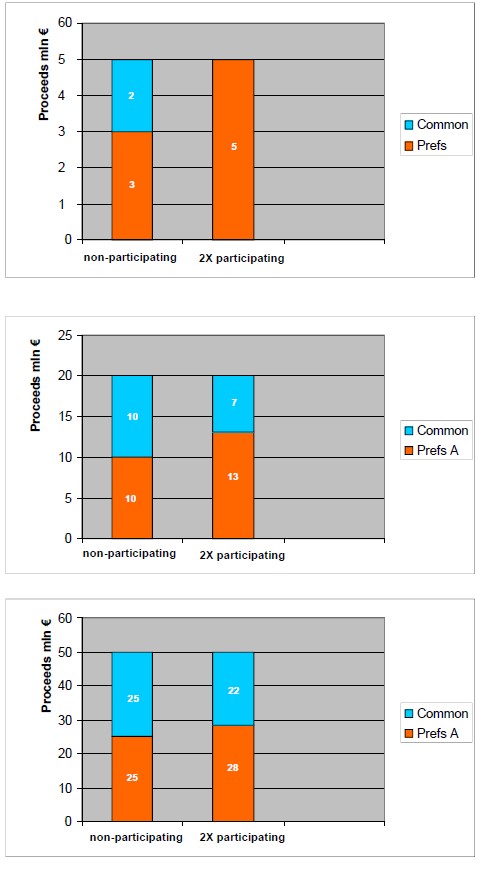

Let’s assume a company is sold for 5 million euro and the preferred shareholders invested 3 million euros, holding a 50 percent equity stake, with a 2x participating liquidation preference. It is clear that this results in proceeds flowing to the preferred shareholders. If the proceeds were 20 million euros, the investors would get 6 million plus 50 percent of the remaining proceeds, resulting in 13 million in total for the investors and 7 million for the founders.

If the proceeds were 50 million, the investors would get 6 million plus 50 percent of 44 million, resulting in 28 million for the investors and 22 million for the founders. If it was a non-participating liquidation preference with a conversion right, at the 5 million euro sale, the proceeds would be shared 3 million for the investors, 2 million for the founders. At a 20 million euros sale, the preferred shareholders would convert and the proceeds would be shared 10 million each. At a 50 million euro sale, the proceeds would be shared 25 million each.

To make this more visible, I’ve put these numbers in the simple graphs below (click to enlarge). As you can see, when the exit proceeds rise, the effects of participating liquidation preferences in comparison with non-participating liquidation preferences decrease.

Graphics based on the ones included in Venture Capital Term Sheets, Harm F. de Vries & Menno J. van Loon, 2005 Reed Business Information

What is commonly used?

Which liquidation preferences are commonly used depends on market conditions and bargaining power of the parties, but generally speaking in Dutch seed or series A deals it is usually either a simple liquidation preference with a conversion right (or similar, see above) for the investor or a capped or non-capped 1x participating liquidation preference. Multiples like 2x or 3x participating liquidation preferences are not common at all.

Most investors will not want to burden a company with excessive liquidation preferences, but instead are seeking for a reasonable compromise. Excessive liquidation preferences are not motivating for management and employees, which in the end is also not in the interest of the investors.

Finally, seed and early stage investors should be careful with asking for excessive liquidation preferences, since they may shoot themselves in the foot. Investors who invest in later rounds will require at least the same rights that the existing shareholders have.

Moreover, later stage investors usually want their preferred shares to rank senior to the earlier investors: series C gets its preference first, then series B, etc. This might result in a situation where the holders of preferred shares issued in later rounds get everything and the seed investors, who started this ‘thing’, are last in line and get nothing.

Image credit: Patung Dewa Ruci (Flickr)

Sjoerd Mol is attorney-at-law at Benvalor. He has been an attorney since 2003, specializing in corporate law and mergers & acquisitions. His clients include start-up businesses, Dutch and foreign companies, private investors, family offices and investment funds. Reach out via mol@benvalor.com

Hi Sjoerd, thanks for this excellent article. I really liked your remark about early investors shooting themselves in the foot: I often see one early investor asking for better terms and conditions than other investors, not realizing that this opens the door for other people to ask for special terms and conditions as well. In the end, everyone is confused and nobody benefits. Let’s hope we can keep Dutch investment term sheets nice and simple, so everyone can focus on the business

I fully agree that simple is the way to go, and we always strive to do so. There are circumstances, however, where a more agressive participating pref helps to bridge a valuation expectation gap. This for me is another part of the puzzle. A more realistic valuation often solves the need for participating preferreds. In lifescience investments they are also more prevalent n in tech.

Final comment: if VC funding dries up further I would not be surprised to see more participating preferreds popping up as well